UnitedHealth Stock Analysis 2025 – Is UNH Undervalued?

Intro: UnitedHealth Stock Analysis 2025

“The sky is falling!” shouted Chicken Little. Chicken Little was one of my favorite books growing up, as it teaches two valuable lessons: (1) Do not panic without verifiable proof; Chicken Little was convinced the sky was falling after just a single acorn hit him in the head; and (2) Mass hysteria is dangerous; his panic spread to others (i.e. Henny Penny, Ducky Lucky, etc.), illustrating how fear can engulf groups without reason. Alright, enough about children’s fables; So, what does this have to do with determining if United Healthcare’s (UNH) stock is undervalued?

Well as investors, we also may be exposed to similar societal patterns of overreaction to negative news; such instances echo the magic 5 to 1 ratio Dr. John Gottman infamously spoke of: For every one negative interaction during conflict, a stable and happy relationship needs five (or more) positive interactions. At times, the market tends to also overreact in this way to negative news. For investors willing remain rational and put do the research, such times of negative market sentiment may breed significant opportunities, which an investor can exploit.

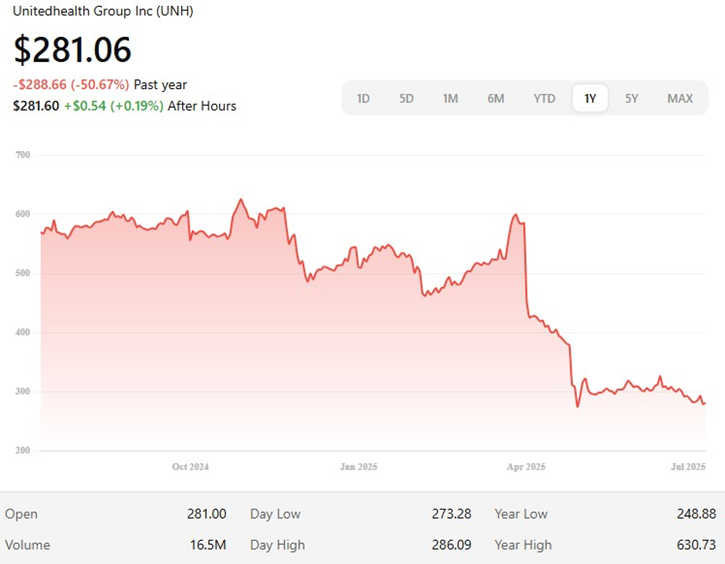

So, is UNH undervalued? In this Weekly Investments analysis, we’ll apply the above mindset to UnitedHealth Group (NYSE: UNH). UnitedHealth’s stock has plunged over 50% from its late-2024 highs (around $615) to roughly $283 today. Due to the speed and scale of its rapid decline, investors are standing by fearing the worst. Just as we did in past articles (e.g. META and DAC during their own turmoil), we will evaluate whether UnitedHealth’s plunge is a case of Chicken Little style of market overreaction or if the pessimism is truly justified by the fundamentals.

Business Overview & Recent Turmoil

Overview: UnitedHealth Group (NYSE: UNH) headquartered in Eden Prairie, Minnesota, is the largest healthcare company in terms of revenue among global competitors. The company operates within two main segments: UnitedHealthcare (insurance) and Optum (PBM, health services, care delivery, etc.). As of July 28, 2025, UNH’s market capitalization stood at roughly $255 billion (significantly down from the approximately $567 billion market cap it reached at its peak in November 2024). Through Q1 2025, revenue for the company has grown at roughly a 11.78% CAGR over the past ten years while free cash flow grew at 12.78% during the same period. UNH pays a dividend of about 3.17% per year which has grown steadily over that last ten years by 15.98% CAGR. UNH’s next earnings report will be for Q2, 2025 which will be released on July 29th 2025 before market open. We have chosen to publish this article a couple hours before the Q2 2025 earnings release as we expect management to be able to add additional clarification to details discussed within; in addition to a potential market reaction which could result in an even more advantageous buying opportunity.

UnitedHealth’s Recent Woes: UnitedHealth’s fall from grace has been both swift and dramatic. UnitedHealth’s stock is down roughly 44% year-to-date and approximately 50% in the last twelve months. It seems ever since the December 2024 killing of UnitedHealthcare’s CEO Brian Thompson, this company cannot catch a break. A few of the contributing factors which led to this loss of investor confidence include:

- DOJ confirmed a criminal and civil investigation into United Healthcare’s Medicare billing practices in late July 2025 (a potential civil investigation was first reported by WSJ in February 2025).

- Unexpected medical utilization costs experienced significant increases throughout the industry.

- CEO Andrew Witty resigned and was replaced by chairman Stephen Hemsley.

- President Trump issued executive orders with an attempt to establish MFN (Most Favored Nation) pricing on pharmaceuticals.

- UNH experienced it first earnings miss in Q1 2025 since 2008.

- $1 trillion of cuts to federal Medicaid funding were announced as a result of the new Tax Bill.

- UNH suspended all earnings guidance on May 13, 2025 after the company had already cut its EPS forecast by about 12% from $29.50-$30.00 to $26.00-$26.50 in mid-April 2025.

Given surging medical costs, spiking MLRs, leadership upheaval, and political/regulatory clouds on the horizon (which we’ll detail shortly), its no wonder why investors may feel as if the sky may be falling. Let’s now examine UnitedHealth’s opportunities, risks, and fundamentals further to determine if we believe the pessimism from the recent selloff is warranted or if this has created an investment opportunity. Catalysts which we will consider will be opportunities which will assist UNH in its recovery and risk factors which potentially may keep UNH’s stock price depressed. Lastly, we will provide comparisons to past events and valuations, to assist in estimating a valuation based on historical multiples.

Five Opportunities for UnitedHealth’s Long-Term Outlook

1. Shareholder Returns: Buybacks at Bargain Prices and a 3% Dividend (Probability: High; Impact: Medium-High):

In 2024, UnitedHealth returned over $16 billion to shareholders via share buybacks and dividends. One silver lining of UNH’s recent troubles, is that the company is notorious for returning shareholder value via share repurchases; The company bought back approximately $9 billion of its own stock in 2024 and $8 billion in 2023. At the current market cap of $255 billion, $9 billion worth of share repurchases equates to roughly 3.52% of shares being retired annually; conversely if this plunge in share price had not occurred, and the company bought back $9 billion shares at a $567 billion market cap (peak November 2024), they’d only be retiring 1.59% of outstanding shares per year. As illustrated, UNH is essentially repurchasing shares at a BOGO (buy-on-get-one free) discount in comparison to 2024 prices. Share repurchases play a significant role in returning value to shareholders; when buybacks occur, the value per share increases via the retirement of shares outstanding (less ownership interest outstanding) while also circumventing shareholders having to pay income taxes on distributed dividends (hints why Warren Buffet’s Berkshire Hathaway hasn’t paid a dividend since 1967)

As mentioned above, share repurchases aren’t the only way UNH returns value to shareholders. UnitedHealth currently sports a 3.15% dividend yield with a payout ratio of 31.71% of FCF. To put this into perspective, UNH’s average dividend yield over the last 10 years is 1.63%. Also for comparison, UNH competitors’ yields currently sit at: Elevance Health (ELV): 2.37%, Humana (HUM): 1.49%, and Centene (CNC): 0%.

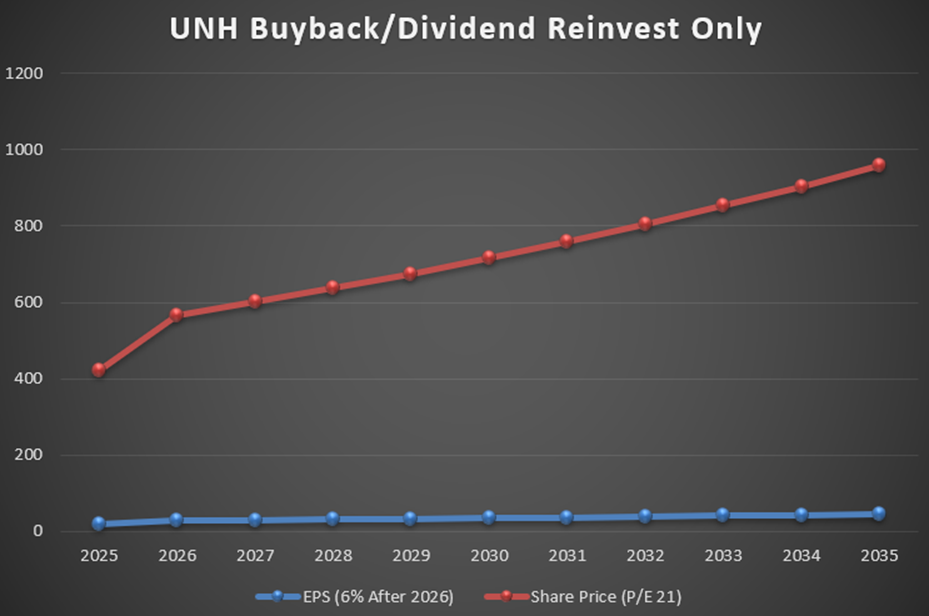

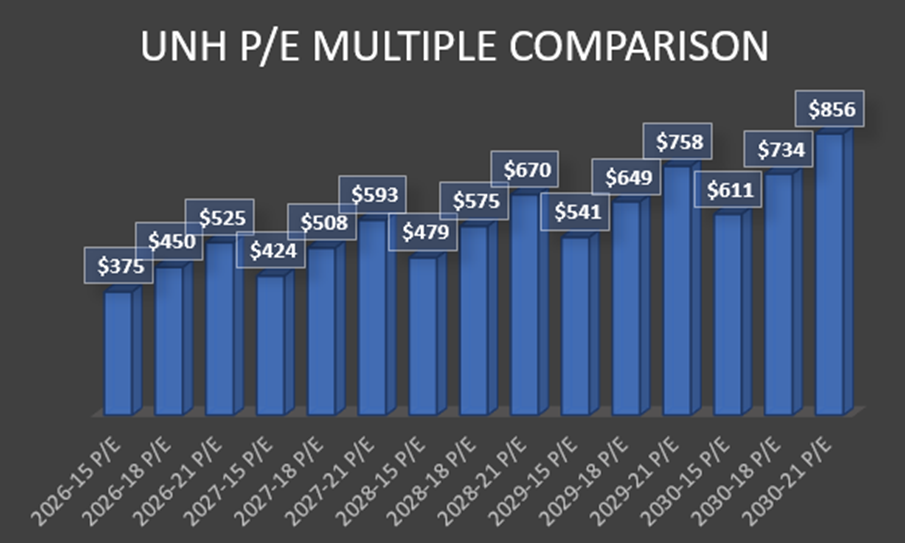

For a visual representation of the impact these buybacks and dividends would have on earnings and ultimately share price, refer to Exhibit -3 below. Note: this is just so one can visualize the impact of the repurchases/dividends and these aren’t our actual price forecasts. For the following graph we will make the following assumptions: UNH growth becomes stagnant (0%) after 2026 but continues to retire 3.5% shares annually, EPS is $20 in 2025 (will further elaborate on this assumption in the following sections) but normalizes to $27 EPS in 2026, the shareholder reinvests the 2.5% dividend yield (omits 0.5% for dividend taxes paid by the recipient), and a P/E ratio of 21 (10 year average p/e is 25.04).

There are a handful of assumptions and inputs missing in this graph; the sole purpose is to provide a visualization of the significant impacts buybacks (at current rates) and dividends reinvested can have; all-the-while omitting any additional external growth.

2. Strong Tailwinds in Medicare Advantage Rates (Probability: High; Impact: High):

UNH is by far the nation’s largest Medicare Advantage insurer. Health Insurers recently struck a solid deal with the Trump administration which includes a 5.06% hike in MA plan rates in 2026; well above the 2.2% increase the Biden administration initially proposed in January 2025. United Healthcare’s Medical and Retirement segment (includes Medicare Advantage plans) made up approximately 25% of UNH revenue ($139.5 billion) in 2024. Bottom line: UnitedHealth will be repricing its MA premiums for 2026 to catch up with the recent cost surge (discussed in sections to follow), coupled with CMS handing out their newly increased benchmarks. These changes will play a crucial role in stabilizing MLR and restoring profitability margins to pre-2025 levels.

3. Aggressive Cost Management & AI Efficiencies (Probability: High; Impact: Medium):

UnitedHealth’s management has communicated they will be responding to the ongoing margin pressures by intensifying their focus on cost reduction; in particular exploring further efficiencies utilizing AI. For example, Optum RX cut onboarding costs by 9% in 2024 alone through digital automation. On a July 2024 call, former CEO Witty commented there being “hundreds of AI use cases” being implemented to make operations more efficient. Such efficiencies and cost savings are on display when viewing the company’s most recent quarterly release. The Q1 2025 operating cost ratio improved fairly significantly to 12.4% in comparison to 14.1% a year ago. The company went on to attribute the favorable margins to “increased technological and other operating efficiencies across UnitedHealthcare and Optum.”

Given UnitedHealth’s massive scale (approximately 400,000 employees), even a small percentage of improvements translate to billions in savings. In short, the company is utilizing AI in order to trim the fat; this bodes well for next year’s earnings recovery. These cost cuts are impactful but they do have limitations; it is great to see UNH is exploring ways to create additional shareholder value, but these automations will eventually run into a wall of finite returns.

4. Diversified Growth Engine in Optum (Probability: High; Impact: High):

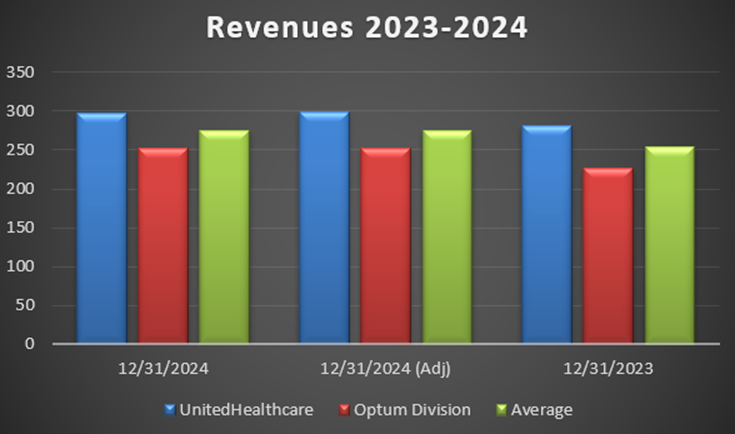

The real driving force in recent years regarding UnitedHealth’s growth is it’s Optum division which includes Optum Health for care delivery, Optum Insight for data/analytics, and Optum Rx for pharmacy benefits. Optum has allowed UNH to vertically integrate its product offerings far beyond the typical insurance provider. In addition to the diversification, in recent years it has seen solid growth; In 2024, the Optum division experienced a 12% year-over-year growth which equated to full year revenues of $253 billion ($26.3 billion increase from prior year). Optum Rx (UnitedHealth’s PBM) saw revenues increase 15% year-over-year. Optum Health (revenues grew to $105.4 billion in 2024) has steady been acquiring and partnering with care providers (e.g. clinics, surgery centers, home health agencies, etc.) which led to servicing 4.7 million people in value-based arrangements by the end of 2024; UNH expects this to grow by an additional 650,000 patients in 2025.

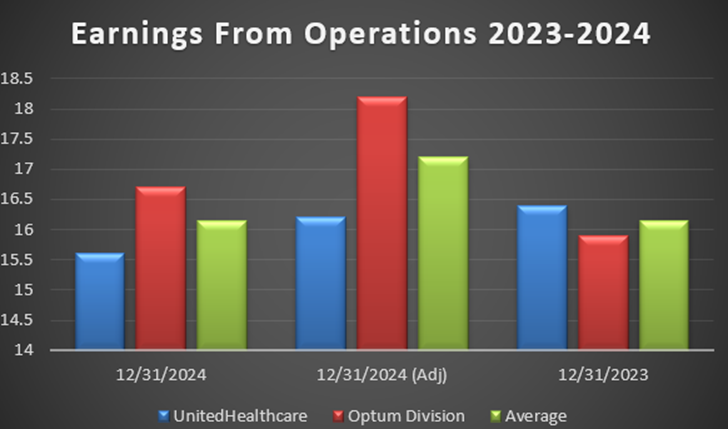

The Optum division at UnitedHealth not only brings in almost half the company’s revenue, but also is made up of higher margin segments in comparison to a typical healthcare insurance provider. The below graphs will provide a representation of how Optum’s margins create operating earnings which exceed the UnitedHealthcare division earnings.

Disclosure: Earnings growth at UnitedHealth is largely dependent on the ongoing regulatory pressures regarding healthcare providers and in particular PBMs. We discuss regulatory pressures further in the following section on potential weakness.

5. Valuation at Multi-Year Lows (Probability: High; Impact: High):

As mentioned previously, UNH is down roughly 50% in the past twelve months. The stock is currently trading at a forward P/E of 12.67 (our own estimate which we will discuss below; much of the current online data appears to be understating P/E as it has yet to be updated since UNH pulled its guidance). So, the question remains, has this selloff been overdone? Is UNH stock undervalued? The following example will explore simple valuation multiples to determine future price points by utilizing current vs. historic ratios.

Assumptions: To begin, we must first accept that 2025 earnings will likely be a negative outlier on earnings for all major health insurers as they all vastly underestimated medical costs (discussed in detail in the below section on potential weaknesses). A caveat regarding this issue though is that it almost certainly will be short lived (FY2025). Assuming other factors remain consistent, 2026 earnings should mostly return to 2024 norms; therefore, since the company remains cash flow positive and financially sound (not taking on debt to finance losses), it would be reckless to assume future earnings will continue to be in line with 2025; therefore, our valuation models for 2026 and beyond will be comprised of conservative estimates based off UNH’s 2024 financials.

Furthermore, due to UnitedHealth being in a defensive sector, consistent premiums including float to invest, difficult barriers to entry within the healthcare industry, past premium valuation multiples, economies of scale, and UnitedHealth’s industry dominance, this will be one of the few instances we stray away from Warren Buffet’s cigar butt method of value investing and believe it appropriate to place a premium expectation on the future stock price greater than our normal ceiling of a forward P/E of 15.

Details: Over the last ten years, UNH has sported an average P/E ratio of 25.04. Its forward P/E is fairly unknown due to the current hiccup year resulting from significant MLR increases along with the company pulling its guidance; therefore, to estimate a forward P/E for UNH, we will assume the following: the last two quarters of 2025 will end up with average of $4.50 EPS (conservative estimates) while the first two quarters of 2026 will return to the 2024 norm ($6.75 per quarter). With these assumptions in place, total earnings for the next four quarters would be $22.5. At a share price of roughly $285, that’s a forward P/E of 12.67. Note: if and when costs stabilize, earnings should return to the norm (all else remaining consistent) and P/E will steadily decline until price decides to catch up. For instance, $27 eps in 2026 at $285 share price equates to a 10.56 P/E.

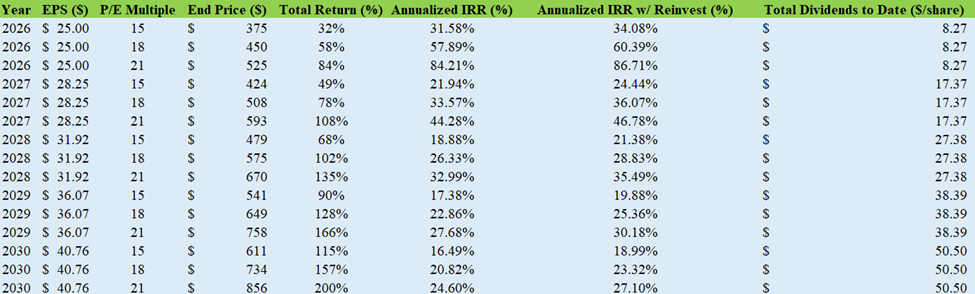

Now let’s assume the following: the market’s worst fears do not fully materialize and earnings return to a conservative norm of $25 EPS in 2026 (vs. $27+ Adjusted EPS 2024), earnings grow at 13% over the next five years (vs. 16.72% 10-year average), and we will use conservative P/E pricing multiples of 15, 18 and 21 (vs. 25.04 avg. P/E for the last ten years). Lastly let’s assume the investor acquires shares today for an average price of $285 per share. Refer to Exhibit -7 below for a visual representation.

The above chart also includes columns for dividends per share and annualized IRR if dividends are reinvested. Let’s assume we bought into UNH today at the average price of $285. In mid-2027 after all the dust settles, we decide to sell at a conservative P/E multiple of 18; given that multiple, the stock would sell for $508. This would net a 78% total return and an annualized IRR on the initial investment of roughly 34%. It’s important to point out, that $508 does not include the $8+ annual dividends the shareholder would be collecting in the meantime equating to roughly $17.

Obviously the above is not our typical preferred method of valuation as we usually favor utilizing customizable variations of DCF, FCF, Graham formula and Peter Lynch pricing formulas to approximate a reasonable value and establish an appropriate margin of safety. That being said, there are rare occasions when a stalwart has come to our attention when we utilize historical ratio multiples in helping determine a valuation. The above isn’t our finalized valuation, but I do believe it depicts the best comparison of the bunch in order for the reader to fully digest and compare the severity of the recent drop in share price.

Lastly, I will leave you with one last historical comparison. There have been two times in the last 20 years in which UNH has experience similar corrections (November 2008 peak-to-trough of -72% and March 2020 peak-to-trough of -36%). UNH’s P/E ratio for Q4 2008 ranged from 9.08-9.46 and the price to earnings ratio for March 2020 was 16.92; therefore, these P/E ratios are in the realm of where UNH is currently valued at (forward P/E of 12.67). Wondering what your return would be if you would have bought at the depressed prices during the last corrections? Glad you asked. Refer to the below chart:

In either scenario, if the investor would have bought near the bottom when shares sported similar valuation multiples as today’s price, he/she would have amounted a total return of 110%+ within two years; or a roughly 45% average annualized return.

Summary of Opportunistic Factors

In addition to the preceding five positive factors above, there are a few other considerations worth mentioning:

- UnitedHealth’s sheer size allows it significant economies of scale along with bargaining power with both drug manufacturers and providers.

- The return of former CEO Stephen Hemsley is a good signal from the company, highlighting its attempt to reestablish investor trust and confidence (Hemsley served as CEO of UNH during its ‘golden age’: 2006-2017). Hemsley didn’t just return, he immediately put his money where his mouth is and purchased $25 million worth of UNH shares.

- UNH is largely diversified in both customer base (e.g. employers, individuals, Medicaid, Medicare, etc.) and services provided (e.g. PBM, Insurance, health services, etc.)

- UnitedHealth has navigated stormy waters before (e.g. ACA regulations, Obamacare Rollout, COVID, Hackers, DOJ investigations, etc.) while continuing to provide 10%+ averaged annualized EPS growth.

In summary, UnitedHealth’s fundamentals remain intact. The company will likely experience strong tailwinds from increased Medicare Advantage rates beginning next year, has a highly profitable steady growing business division in Optum, is proactively cutting costs via implementation of AI, and has continued to award shareholders via dividends/buyback. Due to these factors, it is my belief that the market has pulled a “Chicken Little” type of overreaction which has created an attractive entry point for long-term investors.

5 Major Risk Factors and Challenges Ahead

Well it can’t all be rainbows and butterflies or this wouldn’t be an analysis. UNH does face some real risk factors which justify some caution and understanding prior to investing. Below are five considerations an investor should be aware of.

1. Political and Regulatory Pressure (Probability: Medium; Impact: High):

Newly proposed changes to the healthcare industry and recently adopted regulations are two of the biggest challenges UNH will face in the coming years. In May 2025, President Trump signed an executive order which included the idea of what has been dubbed “Most-Favored-Nation” (MFN) Drug Pricing. In theory, MFN pricing results in the purchasing party paying a price no greater than the lowest price charged to other developed nations.

On the surface, one may speculate this could actually benefit insurance providers as lower drug prices equate to less healthcare insurance providers have to pay out; and such speculation wouldn’t be wrong. That being said, there is one caveat for UnitedHealth and it’s located within their Optum division. The implementation of MFN pricing would likely result in a net negative for UNH as the company is not only a health insurance provider but also a pharmacy benefits manager (PBM). PBM’s remain under heavy scrutiny on capital hill as the benefit managers are being labeled as an unnecessary middleman between insurance providers, drug manufactures, and pharmacies. PBM’s produce income in a variety of ways but one of these ways is by negotiating prices between providers, pharmacies, and drug manufactures; this usually results with the PBM retaining a spread (typically in the form of a rebate). If MFN pricing does fully go into effect, some of the services PBMs currently provide may no longer be needed such as negotiating prices; however, PBMs do offer services beyond negotiating pricing (e.g. administration services, etc.)

The FTC and congress have been relentless in their pursuit to reel in major PBMs. Most of the scrutiny stems from what they have deemed as a lack of transparency in pricing (i.e. rebates) and a conflict of interest from vertically integrated corporations such as UNH; UnitedHealth who owns OptumRx (PBM), OptumHealth (service provider), and UnitedHealthcare (insurer). After feeling the pressure, in January 2025, UnitedHealth released a statement that it would slowly begin the process of passing along 100% of rebates to customers (the company noted they currently pass 98% of rebates to its customers) with plans to have these changes fully implemented by 2028; therefore, the most impactful part of both Trump’s executive order and regulatory scrutiny has already been addressed by UNH. Silver lining: This isn’t the first time the Trump administration has attempted MFN pricing via executive order. In 2020, Trump signed an executive order which was eerily similar. What happened next? It was blocked by the courts for exceeding statutory authority and bypassing required procedures

2. Surge in Medical Costs & Elevated MLR (Probability: High; Impact: Medium):

The primary culprit attributed to UnitedHealth’s first earnings miss in seventeen years (Q1 2025) was the rapid increase in unexpected medical utilization costs. Health insurance providers as a whole, dramatically underestimated 2025 medical costs. Each year around June, health insurance providers submit their pricing and plan rates (i.e. Medicare Advantage, ACA, etc.) for the upcoming year. Once submitted and accepted, these rates are locked in for the entire next year; even if medical expense trends shift dramatically within that timeframe. Health insurers submitted 2025 rates in June 2024. Since their submissions, there has been significant increases in medical utilization rates. This was on full display on July 25th when Centene (CNC) reported Q2 2025 earnings; this release included a Q2 health benefits ratio (i.e. Medical Loss Ratio) of 93% which was a significant increase from the 87.6% Centene reported in the same quarter one year earlier.

As for UnitedHealth, first signs of rising medical utilization costs showed up on its Q4 2024 report in which the full year medical loss ratio ended up at 85.5% in comparison to 83.2% in 2023. UNH’s medical loss ratio for the quarter ended 12/31/24 was 87.6% (largest in seven years). To put this into perspective, utilizing data regarding UNH’s 2024 insurance premiums ($308 billion) from its 2024 annual financial statements, every 1% increase in MLR results in a $3.08 billion pre-tax insurance margin drag on their risk-adjusted premium base.

Silver lining: Earnings for the entire health insurance industry will remain under ongoing pressure throughout 2025 due these materially underestimated costs; however, this will likely be short lived as this dramatic cost shift became clear to insurance providers prior to the cutoff for submitting their 2026 updated rates.

3. Ongoing Legal Investigations and Overhangs (Probability: Medium; Impact: Medium):

A DOJ criminal and civil investigation into UnitedHealth’s Medicare Advantage billing practices was confirmed by the company on July 24, 2025. An article published by the WJ regarding a potential criminal investigation was reported accouple months prior on May 14th. The healthcare industry is notorious for its association with lawsuits, DOJ investigations, and probes; as one might expect, seeing that UnitedHealth is the largest healthcare insurance provider, the company is anything but immune to such scrutiny.

There hasn’t been much details released regarding the current investigation aside from potential reasoning behind investigation being in regards to billings within UNH’s Medicare Advantage program. Needless to say, there are some key considerations an investor should consider prior to jumping the gun and writing off UNH due to a DOJ investigation:

- DOJ criminal and civil investigations take a significant amount of time to work their way through the system. For instance, in 2012 UNH had a whistleblower lawsuit filed against it regarding filing false claims. It took until 2017 for the DOJ to get involved, and just earlier this year (March 2025), the court dismissed the case in favor of United Healthcare; stating the government lacked sufficient evidence. The DOJ responded in April 2025 by filing a motion opposing the dismissal which should be ruled on later this summer. The point is, beginning with the initial lawsuit filing date, it took five years for DOJ to get involved (where current investigation stands today) and once the DOJ did get involved, it took approximately eight years for a ruling to be rendered (yet it’s technically still in the courts given the appeal by DOJ). Based on our research this timeframe is reasonably in line with other industry related DOJ probes/investigations. Also, why hasn’t this $2 billion fraud case from 2012 been lingering over UNH investor sentiment for the last 10+ years? Likely because the negative investor sentiment was short lived and ultimately investors believing even if a loss is recognized, it’s a small cost of doing business.

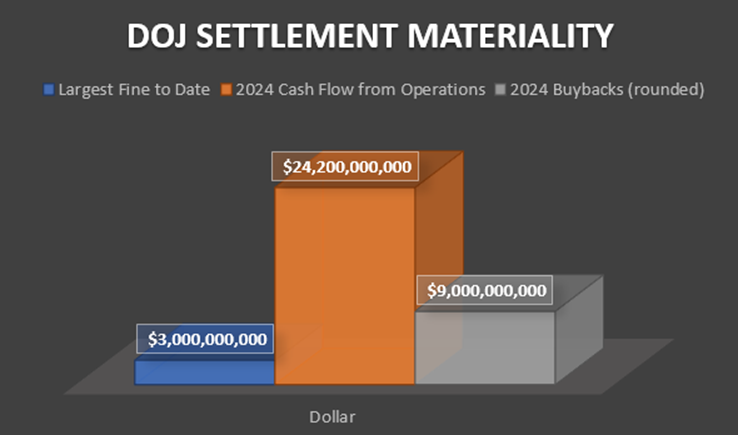

- The largest healthcare related fine/settlement for an individual company stemming from a DOJ investigation was a $3 billion fine in 2012 to GlaxoSmithKline. Why does this matter? It provides a baseline for a worst-case scenario. Yes, I recognize $3 billion sounds like a lot of money; but in the grand scheme of things, it’s simply an expensive speeding ticket to a company the size of UnitedHealth. To put into perspective, the company buys back roughly $8-12billion of its own stock a year and currently sports an annual adjusted income of $22billion+ (with FCF>Earnings). At current prices, if the company were to use that $3 billion to buy back shares, it would retire roughly 1.1% of shares outstanding ; with this in mind, the rational investor must ask oneself, does this probe alone warrant a 40%+ drop in share price since the original WSJ release?

To summarize, even if UNH received a fine equal to the LARGEST healthcare DOJ settlement/fine ever ($3 billion), it almost certainly wouldn’t be paid until 2029 at the earliest (aside from any rushed resolution by UNH working with DOJ); lastly, if the company did have to pay it, it would be a one year hit to EPS of roughly 13.6% current earnings (will gradually become less impactful as time passes and earnings grow).

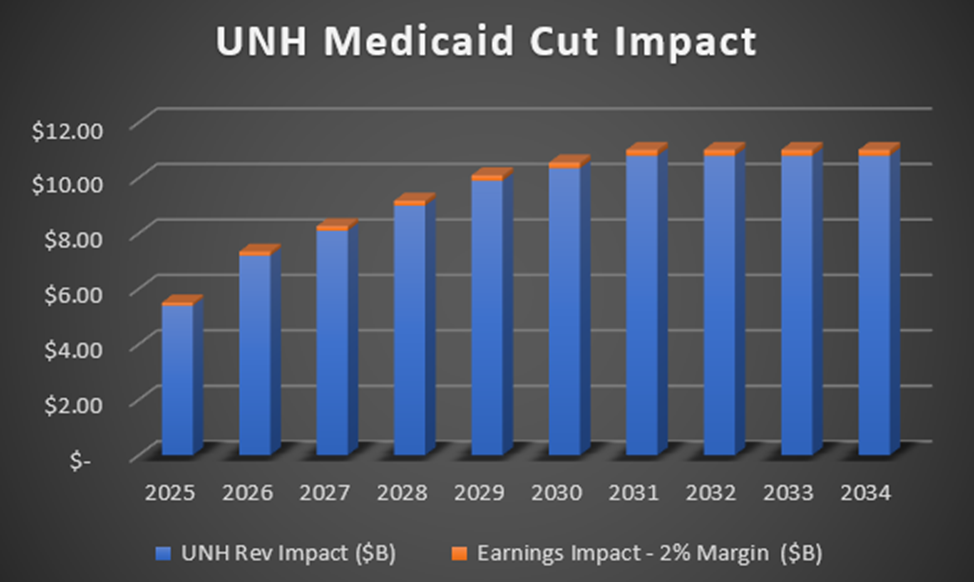

4. Challenges in Medicaid and Other Businesses (Probability: Medium; Impact: Low):

The newly passed Tax Bill which goes into full effect beginning 2026 aims to cut over $1 trillion of Medicaid funding over the next ten years. What does that mean for health insurers? Let’s first confirm a brief understanding how Medicaid works. Medicaid is a joint federal-state program which provides healthcare to low-income families, individuals with disabilities, pregnant mothers, and others in need. How is Medicaid funded? Medicaid is funded through a Federal-State partnership in which the federal government pays a percentage of each State’s Medicaid costs. This is called FMAP (Federal Medical Assistance Percentage). The percentage varies by state but ranges from 50%-78%. For instance, say Missouri has a FMAP of 65%. This means the federal government pays 65% while the state only pays the remaining 35%. I illustrate this to show how significant of a role the federal government plays in Medicaid as many individuals I’ve spoken with believe because the state administers the program, the state is the one footing the bill.

Even prior to the new tax bill, Medicaid was already under fire stemming from the expirations of pandemic-era Medicaid enrollment projects which led to millions of Americans losing coverage via the “redetermination” process. During COVID, states were unable to remove enrollees from their Medicaid program. These regulations have slowly phased out over the last couple years which has led to a drag on revenue for Medicaid MCO providers.

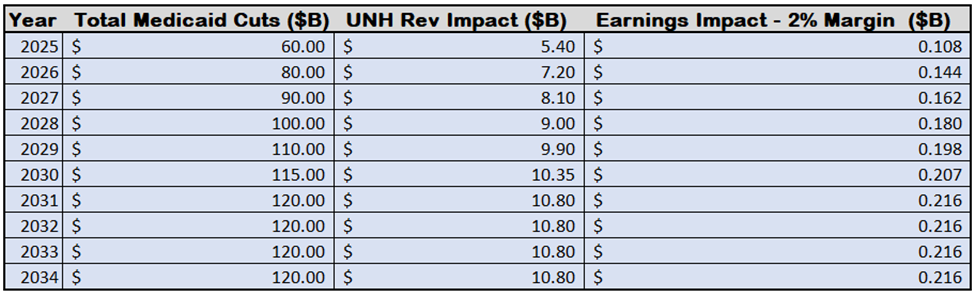

So, what does $1 trillion of Medicaid cuts over the next 10 years look like to UnitedHealth? Luckily for UNH, only roughly 20% of their revenue ($20 billion in Q4, 2024) is derived from Medicaid (“Community & State”). It is worth noting that just because this is 20% of the company’s revenue, this doesn’t translate to 20% of company’s earnings. Medicaid is one of the lowest margin business lines at UnitedHealth; in reality, Medicaid likely makes up closer to 15% (estimated) of its earnings. For comparison, consider Centene (CNC); over 60% of the company’s revenue stems from Medicaid backed programs.

For a visual representation and analysis (Exhibit-10) of estimated overall impact these cuts may have on UNH earnings, let us begin with the following assumptions:

- UNH owns a 9% market share of the Medicaid MCO market

- Medicaid cuts are proportionally distributed based upon each company’s market share

- UNH’s Medicaid net margin on such a low margin product is 2%.

- Annual Medicaid cuts follow the estimates in the second column of Exhibit-11 below labeled “Total Medicaid Cuts ($B).

In 2034, the Medicaid cuts will be fully implemented and finalized; the estimated total impact on UNH earnings will be approximately $1.863 billion in total lost earnings which will be spread over a ten-year period; this is de minimis to a company the size of UNH.

Conclusion: In response to these federal cuts, I foresee a handful of states expanding their own funding of these programs via additional taxes and/or other forms of additional revenue to compensation for some (but not all) of this lost coverage.

5. Other Notable Risks (Probability: Medium; Impact: Low):

Some of the other notable risks one should consider are macroeconomic conditions (such as a recession putting a strain on commercial membership; even though healthcare has historically been a defensive sector), public sentiment (UNH will need to continue its reputation and rebranding efforts following the cyberattack last year along with the negative publicity gained after the execution of CEO Brian Thompson), and additional tax/regulatory updates (e.g. such as the 1% excise tax on buybacks).

After weighing all these risk factors, it’s clear that UnitedHealth does face some serious hurdles. The next few quarters may be quite volatile if the company is unable to stabilize MLR and/or silence the noise around new regulations/investigations. That being said, UnitedHealth has navigated these waters before and has consistently shown perseverance. The company has a solid track record of being flexible and quick to adapt to change (e.g. AI integration, 100% customer rebate commitment, etc.).

Conclusion:

So back to the original question: Is UNH undervalued or is the sentiment around “the Sky is Falling” accurate? I believe the significant drop in share price has produced a solid opportunity for long-term investors to purchase a well-established company located in a defensive sector which sports consistent growth at a discounted price. I also think this hiccup may benefit long-term shareholders as UNH is buying back billions of dollars of shares at half the price they were paying less than one year ago. It is for these reasons coupled with the details listed above, I would rate UnitedHealth (UNH) a BUY with a one-year price target of $401 (conservative DCF) and a margin of safety of 29%.

Considerations: The investor should take into consideration, he/she should have a long-term investment horizon in mind (minimum 12+ months) as 2025 will be a wash due to premium costs already being locked in for the year. A company fundamental turnaround will not likely be confirmed until at the earliest mid-to-late April 2026 (Q1 2026 earnings release); as this will be first time investors will get a glance at the benefits of the increases in Medicare Advantage rates (5.06%) coupled with the updated cost structure; meanwhile, the investor can sit back and collect a 3%+ dividend while enjoying a significant amount of share repurchases at these suppressed prices.

Disclosure

This article is for informational purposes only and does not constitute financial or investment advice. The views expressed are those of the contributor and are based on publicly available information and personal analysis.

The contributor holds positions in some of the investments mentioned, including UnitedHealthcare Group (UNH), Centene (CNC), and may benefit from any price appreciation discussed herein. This potential conflict of interest is disclosed for transparency.

No representation is made as to the accuracy or completeness of the information provided. Readers are solely responsible for verifying any facts and should consult a licensed financial advisor before making investment decisions. Past performance is not indicative of future results.