Danaos Stock Price is Undervalued: 15 Reasons Why DAC Stock Price is Undervalued

Background Danaos:

Danaos (DAC ticker) is one of the largest owners of containerships worldwide; this Greek company is in the business of chartering its containerships at fixed rates to liner companies. We first recommended Danaos in September 2020 when the company was seriously suppressed at roughly $4.60 a share. The reasoning for this recommendation was the company was irrationally being undervalued due to the market failing to recognize a supply shortage of containerships, delays due to COVID causing bottlenecks/congestion at ports, a large COVID related e-commerce boom, companies restocking depleted inventories, and significant undervalued assets which were not being fully accounted for; this included, approximately 10 million shares (10%) of ZIM Integrated Shipping Services which had yet to go public; ZIM was being held on Danaos’ books for roughly $75k. As of the time of this writing (less than a year later), that same 10 million shares of ZIM is now worth approximately $400 million. You read that right, $399 million+ worth of assets were not being recognized by Danaos; all an investor had to do was look. For comparison, the average market cap of Danaos in September 2020 was only roughly $150 million!

Danaos first stood out by how well the managed it was in comparison to competitors; it was even more surprising that the company with better operating margins was trading at a discount compared to peers. Initially this was due to debt and solvency uncertainty; but as the best seller book Rich Dad Poor Dad teaches, there is good debt and bad debt. When a company can use debt (within reason) to invest in fixed assets which retain value and increase earnings greater than borrowing rates (ROIC vs. WACC), this usually is considered good debt. The issue many investors had with Danaos’s debt was it appeared quite risky (to the untrained eye). Do not get me wrong, if charter rates would have remained suppressed and/or global trade stood frozen due to COVID, all shipping companies, including Danaos, would have been in serious trouble; but by September 2020, most of the economy had opened up again. With a little bit of research, one could further realize that the ongoing port congestion would lead to future supply chain issues. Most investors failed to acknowledge the ensuing effects from the increased consumer demand (due to WFH), supply shortages due to port congestion/closures, inflated steel prices, and low interest rates which Danaos would capitalize on by restructuring its debt.

The reason I mention the above is: Many of the same rationales which led to us buying and recommending DAC in September 2020, have not changed (aside from price which we will revisit in our updated valuation below). So there’s only one question left: Is Danaos still undervalued?

Current Day DAC Stock Price and DAC Stock Forecast:

In the past few weeks, Danaos has fallen to under $60 from it’s high of $78+. In my opinion, this drop has created a potential buying opportunity. I am perplexed by the market failing to recognize the following 15 reasons Danaos appears undervalued:

#1) Record Charter Rates

Charter rates are continuing to hit new records almost weekly with 3-4 year charters becoming the norm (pre-COVID charter contracts were much shorter usually only 6-12 months). The shorter the charter length, the more exposure these carriers (i.e Danaos) have to market fluctuations. Also, these longer contracts assist both investors and management to more accurately provide forecasts. Although most carriers are chartering ships for longer periods, some shipowners are taken advantage of the inflated rates by intentionally signing short-term charters. The following article by Freightwaves discusses how a few of these carriers have already been able to charge $100k+ a day. This rapid increase in charter rates coupled with new long-term contracts have caused DAC stock price to return 1000%+ over the past 12 months.

The HARPEX index tracks containership rates for carriers. The graph below from the HARPEX website displays the past one-year change.

Per LloydsList, “Rates are up between 10.7% and 5.5% week on week, and between 45% and 17.4% higher on the month-ago period, and as much as seven times the going rate 12 months ago, according to VHBS.”

Yep, you read that right, as much as SEVEN times the rate only twelve months ago.

#2) Danaos Ownership of ZIM Stock.

Danaos still owns a significant amount of ZIM stock (over 8 million shares after the most recent consolidation – based on my calculations). ZIM currently trades at roughly $38 and is paying out a $2 dividend in August 2021. The company has said it has plans to by 30-50% of 2021 net income in 2022. The 2021 EPS estimate for ZIM according to MarketWatch is $18.17. If Danaos still owns roughly 8 million+ shares, Danaos will receive $16 million in dividends in August 2021 and using the average of 40% earnings (40% x EPS $18.17)= $7.27 per share dividend in 2022; therefore, just from dividends in ZIM within the next year and a half, Danaos will be receive approximately $74 million ($9.27 * 8 million shares). Note: this isn’t taking into consideration if DAC sells any shares.

#3) Danaos Dividend Reimplementation

Danaos reimplemented a $2 annual dividend which at the current DAC stock price of roughly $60, dividend yield is 3%+. Some investors have complained this dividend isn’t as much as its peers; but take into consideration the average SP500 dividend as of June 2021 according to YCharts is roughly 1.35%. In addition, when a company is employing capital and maintaining solid margins, why would one want to pay additional taxes on dividends? Per Finviz.com, Danaos has a ROE of 38%+. Would the average investor be able to produce 38%+ in alternative investments after paying taxes on these dividends?

#4) Solid/Consistent Management

Management is making solid conservative decisions, staying focused, and seeking further acquisition targets. I appreciate managements dedication to paying down debt and prioritizing solvency over returns. Management has been paying cash for almost all recent containership acquisitions. Given the inflated market environment, I believe management has strategically made good decisions for the ships they have bought (refer to my evaluation of the most recent transaction below). Almost all of these acquired ships have current charters already attached; when these contracts do expire, the containership will likely be rechartered at much higher rates prior to 2023. Note: 2023 is relevant as it is the soonest any of the newbuilds will set sail.

For additional information regarding Danaos’s recent acquisitions, here is a great article on Seeking Alpha.

Evaluating Danaos’s most recent acquisition:

From the press release on Danaos’s webstie, this is what we know:

“Danaos Corporation (the “Company”) (NYSE: DAC) today announced that it has entered into an agreement to acquire six 5,466 TEU container vessels built at Hanjin Subic Bay shipyard en bloc for $260 million (the “Acquisition”). The vessels, which have an average age of 6.8 years, are on time charter contracts to leading liner companies with a weighted average charter duration of approximately 2 years.

The Acquisition will increase the Company’s contracted revenue by approximately $71 million and the Company’s contracted EBITDA by approximately $39 million in total and will be funded by cash at hand, although the Company is evaluating debt financing alternatives to finance part of the purchase price.”

Facts:

Number of Ships: 6

Size of Ships: 5,466 TEU

Avg. Age: 6.8 Years

Total Cost: $260 million

Payment/Financed: Cash

Avg. Charter Duration: 2 years

Additional Contracted Revenue: $71 million

Additional Contracted EBITDA: $39 million

Below are screenshots of my analysis of the transaction, please verify my numbers and recognize I use what I believed to be conservative estimates to maintain a good margin of safety for unforeseen risk:

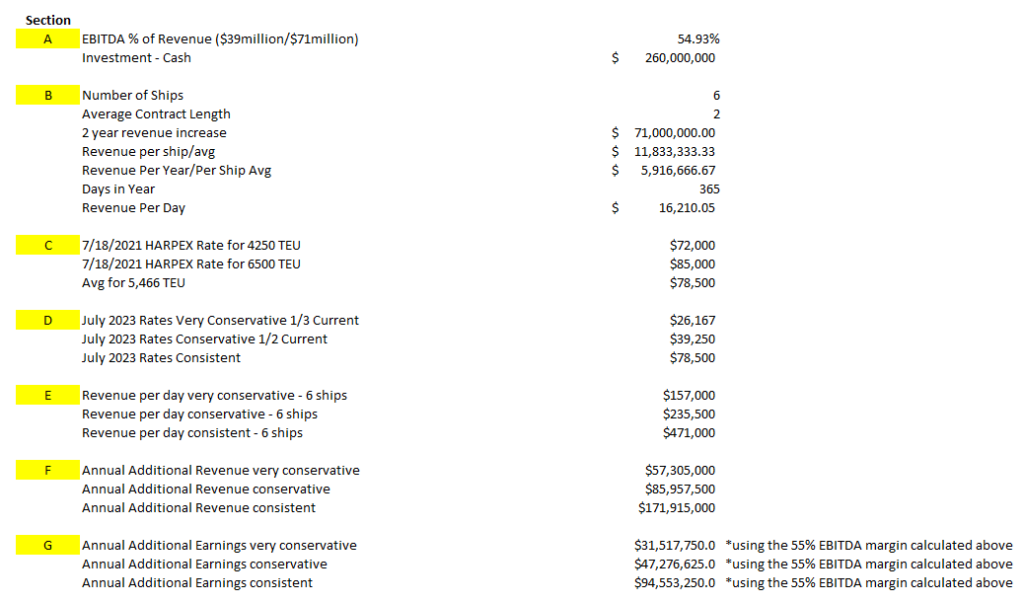

Figure #1:

Figure #1: This breaks out the information provided within the Danaos press release. From our calculations in Section B, it appears the average current charter contract per ship is roughly $16,210 per/day. This means these contracts were likely entered into last year near market bottom. Section C utilizes information from HARPEX which from our calculations puts the present-day average for containerships of similar size around $78,500 per/day. $78,500 vs $16,210, yep you read that right. Since currently near record high rates, Section D’s calculations are conservatively adjusted to calculate what estimated rates for 2023 (average timeframe when rechartering will take place). For instance, line 1 of Section D calculates future rates at one-third of current rates. I believe this is quite conservative and builds in a significant margin of safety (66%). At this conservative rate the average ship will be rechartered at $26,167 per/day which for 6 ships equals roughly $157,000 per/day of revenue (Section E) and about $57,305,000 annual revenue. Utilizing the EBITDA % calculated in Section A of roughly 55%, this would equate to earnings of $31,517,750 per annum.

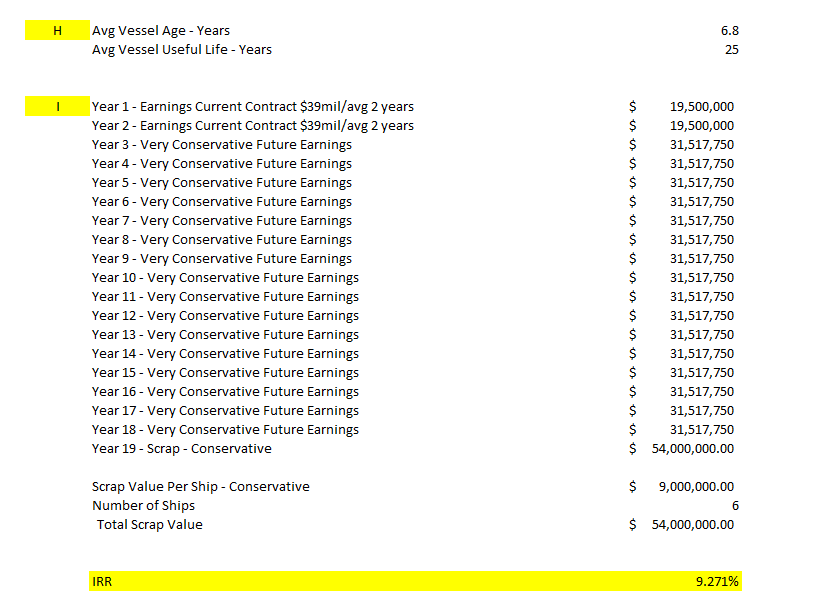

Figure #2

Figure #2: Information sourced from the Danaos press release which lists the average vessel age of 6.8 years. It also assumes a scrap value of $9 million per ship after an average total ship useful life of 25 years. For analysis we will utilize the Internal Rate of Return (IRR) on future cashflows. Since these are conservative estimates with a margin of safety built in, the minimum rate we will be looking for is an internal rate of return greater than a risk-free rate of return (Corporate AAA bond rate – 4%). Note Year 1 and Year 2 earnings have already been contracted: $39 million earnings with an average charter of 2 years ($19.5 million per year). Year 3-18 use the most conservative calculations from Figure #1. After considering annual earnings, scrap value, and the $260 million cash investment, the IRR is 9.271%. I am comfortably pleased with this IRR; not necessary as a current % but largely due to this being a very conservative estimate, which means there is significant upside. Not to mention, company may also choose to refinance these ships down the road to increase IRR.

#5) Healthy Global Trade

COVID kicked off a rapid rise in demand for global trade. Consequently, DAC’s stock price has increase rapidly since then.

According to UNCTAD’s Global Trade Update, the recovery of world trade from the COVID-19 crisis hit records in the first quarter of 2021, increasing by 10% year-over-year and 4% quarter-over-quarter.

Here is great article which references the current condition of global trade.

#6) Marine Shipping Excluded From the Global Minimum Tax Conversation.

The new proposed legislation for a global minimum corporate tax was of concern to the containership industry earlier this year; this is because most carriers do not pay corporate tax due to the counties where they are incorporated. A final agreement is far from finalized but earlier this month it became clear the marine shipping industry will likely be exempt from a global minimum tax.

Although this worried many investors, I personally do not see this as big of a deal as some investors might especially for companies which charter these ships; regardless whether this is imposed on carriers or not, these companies would still be paying close to 0% in taxes after taking into consideration depreciation tax write-offs (think of heavy fixed asset industries such as real estate investors and their depreciation tax write-offs).

This article by Lloyds list discusses this further.

#7) Management has Remained Cautious and Conservative

Management appears to have learned valuable lessons from past market corrections; they have not overleveraged or placed large orders for newbuilds in this expensive environment. Even bad management can look good when things are going well but it’s when the market hits turbulence when investors learn who they have put in the driving seat; for the past decade things have been quite volatile for the containership industry. Through it all, management appears to have remained transparent and consistent. What would be of great concern to me, is if management began to focus on appeasing short-term speculators over long-term shareholders. I do believe Danaos management is focused exclusively on its long-term shareholders. Danaos stock price slid after the Q1 2021 earnings call when management communicated it will be building a “war chest” for unpredictable times and future investments. The short-term fair-weather stockholders were upset; first the speculators wanted to reinstate the annual dividend, once that reinstatement was confirmed, now they are pushing to receive a “special dividend” similar to what ZIM Integrated Shipping is paying out. Reminds me of leaches trying to suck a business dry; then after that special dividend is paid, they will sell. Even after this pressure and the stock taking a short-term hit, management remained unphased and focused on executing their business plan. This is appreciated and displays a management which is directly aligned with long-term company growth and not inflating the stock price for personal gain.

#8) Containership Resale Market – Scrapping/Steel Prices are Extremely High

According to an article by Fortune.com dated July 8, 2021, steel prices have risen 215% since March 2020.

#9) Danaos Q2 Net Asset Value (NAV) Likely Greater than $100 Per Share

According to the Danaos Q1 2021 presentation, the Net Asset Value (NAV) per share was $90.90. With rising steel prices, influx of cash, new acquisitions, and contracted revenues, I believe the NAV for Q2 will easily be $100+ per share. I believe its a bargain to purchase a stock with strong fundamentals and a NAV of $100 when share price is less than $60. Buy your stocks like you buy your groceries, not your perfume.

#10) Danaos Focused on Its Niche: 2,000 TEU-10,000 TEU Containerships

Danaos is clearly focusing on a segment of the containership market that has been ignored; containerships in the 2,000 TEU-10,000 TEU category have hardly seen any newbuilds over the past decade: There are several benefits of containerships of this niche size which the market appears to be ignoring; such as, accessibility to smaller ports, maneuverability, quicker turnaround times to load/unload, and future regulatory uncertainties. I would also argue this diversifies risk for carriers and liners. With a new 20k+ TEU Megamax ship, if a single thing goes wrong such as the Ever Given – Suez Canal situation, there can be serious consequences. Yes, one may argue the chartering company is not liable for many of these potential issues, but when significant damages occur, the finger tends to point in all directions. Also, if one 20k TEU ship is inoperable, that’s 100% of revenue lost every day; in comparison, if you have two 10k TEU ships, and one of them becomes inoperable, the other ship still is bringing in revenue. By specializing in this size, if issues arise with one ship, consequences are not near as severe in comparison to a MegaMax ship. I believe the industry is gradually beginning to recognize the usefulness of these ships; referencing Loyd’s List which mentions 47 second-hand vessels were sold in June 2021 and of that amount 29 were in the feedermax category (of 2,000 to 3,000 teu).

Per Lloyd List’s Article, “They are also commending rates at about $75,000 per day, based on fixtures reported by brokers.”

The 2007-built, 2,741 teu Posen (IMO: 9349887) was chartered for 12 months for $75,000 daily while Interasia Lines took the smaller and younger Hansa Colombo (IMO: 9357781) for three years at a daily rate of $28,000.”

#11) Fairly Predictable Forecasted Revenues

Since charter revenues are based on fixed contracts, cash flows can be reasonably predictable in comparison to other industries. The only significant risk to these contracted revenues is if the liners chartering Danaos containerships stop paying or go bankrupt; I believe this risk in the short-to-mid-term is minimal as these liner companies Danaos charters to are producing record revenues from the inflated rates; even with most new charters on 3-4 year terms, it’d be quite difficult for these high cash producing liners to go bankrupt within this timeframe.

As of the beginning of Q2 2021, my calculations had roughly ⅓ of Danaos containerships being rechartered within the next year. This is huge. Many of those charters were at MUCH lower rates on short-term contracts. These new charters should command significantly higher rates with 3-4 year terms. With the COVID outbreak in China causing more supply chain disruptions going into the peak season, I do not see rates easing until at least Q1 2022 at the earliest.

#12) Government Involvement/Regulation

Some governments are looking into further regulating the transportation industry; this similarilty has been threatened on multiple occasions in the past. Governments and regulators have continuously communicated there isn’t much they can do about shipping as it is the basic economics of supply and demand. I personally believe governments are much more likely to focus on infrastructure such as expanding ports and on port congestion rather than issues further outside their control.

#13) IMO 2020 Potentially Slowing Speeds Down – Decreasing Supply

IMO 2020 has the possibility of slowing down ship speeds to meet carbon regulations. I first read about the slowing of ship speed a few months ago. I was a bit surprised it was the first time I heard about this, and the impacts had not dawned on me earlier. To me, slowing down ship speeds is the same thing as decreasing the market supply of ships. Less trips equals less supply. I believe this is one of the most unaccounted for yet potentially significantly impactful constraints on the industry which could keep rates at inflated levels. If ships are forced to slow down, going off past orderbook data to balance supply and demand would be like comparing apples to oranges.

For an example, let’s say you are moving 40 boxes and have an option to rent a pickup truck which carries 20 boxes and only takes 10 minutes to get to the destination or you can rent 2 pickup trucks which fit 20 boxes each, but they take an hour to get to destination. Obviously, the single pickup truck would be more efficient even though the supply in the latter scenario of 2 trucks appears greater. But isn’t the supply in the scenario of 2 trucks actually greater? Depends on what you are measuring. In both containerships and this example, we have a certain amount of supply needing to be moved but by slowing down the speed at which it moves, this also decreases the amount of supply moved within a specified timeframe. In both cases, the business is transporting fixed amounts of cargo, so the number of boxes moved within a given time period is of much more relevance and impact on a supply shortage than the number of boxes carried or number of vessels/trucks used to carry them.

Why is this relevant? Because container shipping is a cyclical industry which is controlled by rates. Basic economics tells us there are two main ways to increase price: either increase demand or decrease supply. Slowing down ship speeds could certainly decrease the supply of ships available to move cargo; therefore, increasing rates.

Here is an interesting June 2021 article examining the carbon restrictions and potential of slowing down ship speeds.

#14) Insider ownership

Danaos shipping has been a family ran business operating ships since 1972. According to Finviz.com, insider ownership is greater than 50%. This coupled with the fact insiders have not been selling even after the significant rise in price over the past year, tells me they still believe there is value in this stock and at the very least, it is fairly priced.

#15). Port Congestion and Delta Variant

Research shows port congestion persists causing continual delays going into peak season. There are several articles which can explain this further and do a much better job of explaining than I would. Point is, scares from the new COVID Delta Variant may only exhaust an already highly strained supply chain further into the near future.

Considerations and Uncertainties:

Debt

Danaos just recently restructured its debt but still carries a fairly high amount. In comparison to past ratios though, it is quite low, and this company has fixed assets used to secure its debt. Additionally, the majority of this debt is used to buy income producing assets (i.e. containerships).

IMO 2020

This will play a major role in the industry moving forward leaving some uncertainty. As stated in #13 above it may not all have negative impacts especially on charter rates.

Large Orderbook

The current orderbook is roughly almost 20% as of the end of Q2 2021. According to Global Marinetime Hub, the container ship orderbook has more than doubled from a year ago of 9.4%. Even with this increase, the past few years have been near record lows in regard to the active orderbook. Additionally, it will take 2-3 years to build any ships ordered; therefore, there won’t be any relief prior to 2023.

Cyclical Industry

I believe with new contracts terms averaging 3-4 years, liners and carriers both bettering their financial positions, and companies learning from the horrific past decade, rates will not return to previous lows for quite some time…. if ever.

Conclusion – DAC Stock Price and DAC stock forecast:

Based on current charters, my projection of future charters, recent acquisitions, ZIM dividends/settlement of notes, etc. My estimates regarding DAC stock forecast is:

#1 NAV for Q2 2021 will be excess of $100 per share.

#2 My target price for DAC stock price now sits at $96.

This could be a great opportunity for the informed investor to invest prior to the market further recognizing that DAC stock price is undervalued.

DISCLOSURE: I myself and/or affiliates are invested in Danaos DAC stock and/or its affiliates. This article is based on personal interpretations, calculations, and opinions. The validity/accuracy of any information within is not guaranteed. It is the reader’s/user’s sole responsibility to verify/confirm any information from Weekly Investments LLC and/or its affiliates. Although many of these points are supported by 3rd party sources, Weekly Investments LLC does not guarantee the accuracy or validity of information within along with any 3rd party sources and/or affiliates. Weekly Investments and/or affiliates are not investment or tax or legal professionals. Any information should not be taken as investment, tax, legal or any other form of professional advice.