Is GAMB Undervalued? – Gambling.com Stock Analysis 2025

This week, Weekly Investments will be covering why we believe the significant decline in share price of Gambling.com (NASDAQ: GAMB) is overblown. Our 2025 Gambling.com Group stock analysis explores the question on every shareholder’s mind: “Is GAMB undervalued?”

Immediately following reporting Q2 2025 earnings, GAMB stock tanked -17% in a single day and is now down approximately 49% over the last six months. In this article, we will explore whether this correction is warranted and evaluate if this selloff presents a buying opportunity.

Background: Gambling.com Group (GAMB)

Gambling.com Group is a $300 million small-cap company which specializes in digital marketing for customers within the global online gambling industry.

I know what you are probably thinking, “just another sports betting company like DraftKings (DKNG) or Penn National (PENN).” Not exactly. Gambling.com doesn’t operate sportsbooks or casinos; instead GAMB acts as an online affiliate marketer and data provider to those operators.

Gambling.com services include:

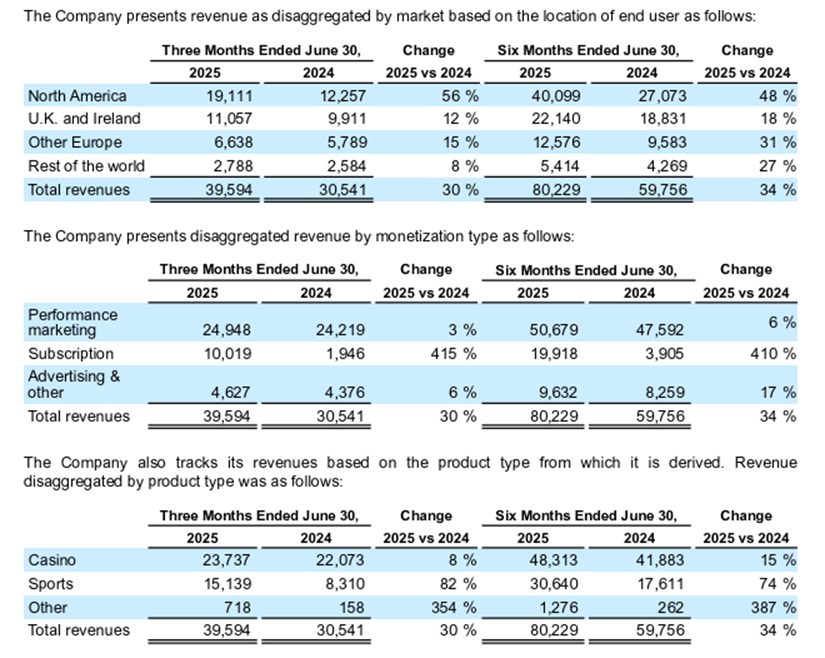

- Affiliate Marketing: Operating through its various brands such as Gambling.com, Bookies.com, and Casinos.com, GAMB specializes in customer acquisition for sportsbooks and casinos. The company earns revenue when it refers customers to these online platforms and those customers in turn are converted into NDCs (new depositing customers). The affiliate marketing business line currently brings in the majority of GAMB revenue (Exhibit-1).

- Sports Data & Tools: GAMB also operates OddsJam (consumer betting analytics) and OpticOdds (B2B data feeds). These rapidly growing platforms largely contribute to Gambling.com Group’s push towards increasing recurring subscription revenue.

Business Model: Instead of assuming the significant risk and capital-intensive nature of owning a sportsbook, this unique asset-light business model is coupled with high margins and scalability; all the while, exposing GAMB to the benefits of a rapidly growing sports betting market.

Headquartered in Dublin with U.S. offices in Charlotte, NC, and Tampa, FL, the company is positioned to continue to benefit from the ongoing legalization of online sports betting in the U.S. along with the growing demand for data-driven betting information.

Below is a breakdown from GAMB’s Q2 2025 report showing the distribution of revenue based on monetization type, product type, and location:

Note: Since GAMB is a foreign private issuer, the company reports under IFRS (International accounting standards) rather than U.S. GAAP. This distinction will become especially important when we begin exploring the Q2 net loss.

Q2 2025 Earnings Release:

GAMB’s share price got absolutely crushed (-17.05%) down to $8.61 on August 14th. In a single day, nearly one-fifth of the company’s market cap went up in flames. At a quick glance, the numbers actually appear quite good:

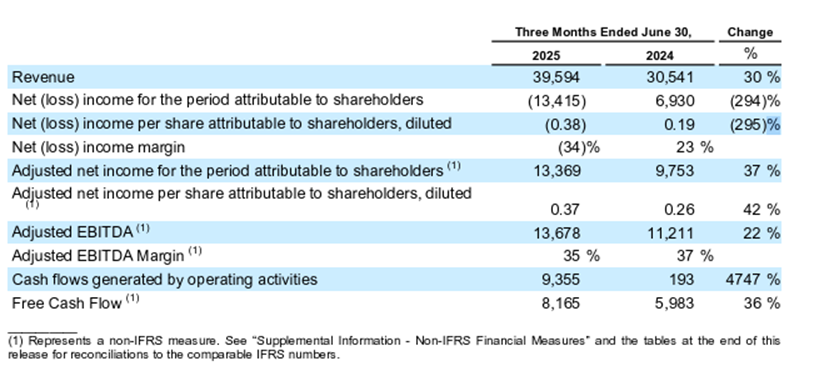

- Revenue: $39.6 million (+30% YoY)

- Gross Profit: $36.9 million (+27% YoY)

- Adjusted EBITDA: $13.7 million (+22% YoY)

- Adjusted EPS: $0.37

Not so bad, right? But here is the catch. Those are the “adjusted” figures which omit contingent consideration (discussed below). On an unadjusted IFRS basis, GAMB reported a -$13.4 million net loss vs the analyst’s expected estimates of +$0.12 EPS. On the surface, posting a loss when the market is expecting a gain, may seem to justify a -17% swing in share price; but that’s where the real story begins.

Despite a few headwinds (e.g. Google rankings, unadjusted net loss, etc.), management reaffirmed the full-year 2025 guidance:

- Revenue: $171–175 million (midpoint +36% YoY)

- Adjusted EBITDA: $62–64 million (midpoint +29% YoY)

What Went Wrong?

The earnings report encompassed several positive catalysts I was hoping to see such as +30% YoY revenue and +27% YoY gross profit. However, I did spot two issues which could be contributing to the continued selloff: Impacts from Google’s June algorithm updates (GAMB temporarily lost some keyword rankings) and the IFRS unadjusted earnings loss.

The impact of Google’s algorithm change is expected to be short lived; on the Q2 earnings call, CEO Charles Gillespie addressed this issue: “Usually, you know, one, two, three months… we should… have it back.” Therefore, this issue should not become a long-term problem.

This leaves the more impactful mention: the IFRS EPS loss. Although this might be a loss on paper, I believe this actually signals good business fundamentals and solid acquisition execution. I will explain why in the following section.

IFRS Accounting – Q2 Net Loss

For the most part, GAMB’s IFRS net loss wasn’t driven by operational weakness or markdowns; rather, it was a non-cash accounting adjustment. To explain further:

- Contingent Consideration (Earnouts): When GAMB acquires a business, the company often structures the deal with contingent consideration (i.e. earnout). These are future payments owed to the sellers if the acquired business exceeds predetermined expectations following the transaction closing. Earnouts are fairly common within M&A.

- When the Business Outperforms: If the business outperforms expectations, which OddsJam and OpticOdds clearly did based on their YoY growth, GAMB must increase a liability on its balance sheet to accrue for the earnout payment it will likely owe in the future (IFRS accounting standards).

- How It’s Reflected on Earnings: The revaluation of the liability is booked as a non-cash expense on the income statement; therefore, this expense still reduces current earnings even though no cash has actually left the business.

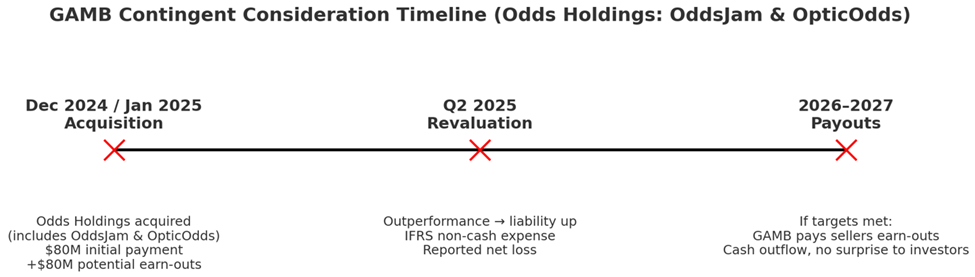

The contingent consideration adjustment recognized in Q2 was related to GAMB’s December 2024 acquisition of Odds Holdings (which includes OddsJam and OpticOdds). The deal was structured with $80 million of original consideration due at closing plus an additional $80 million Odds Holdings would receive based on future business performance through the end of 2026. To earn the full $80 million contingent consideration bonus, Adjusted EBITDA from the acquired Odds Holdings assets would need to more than double for FY 2026 compared to FY 2024.

Exhibit-3 below is an example to help visualize an earnout:

IFRS Accounting Treatment – Contingent Consideration

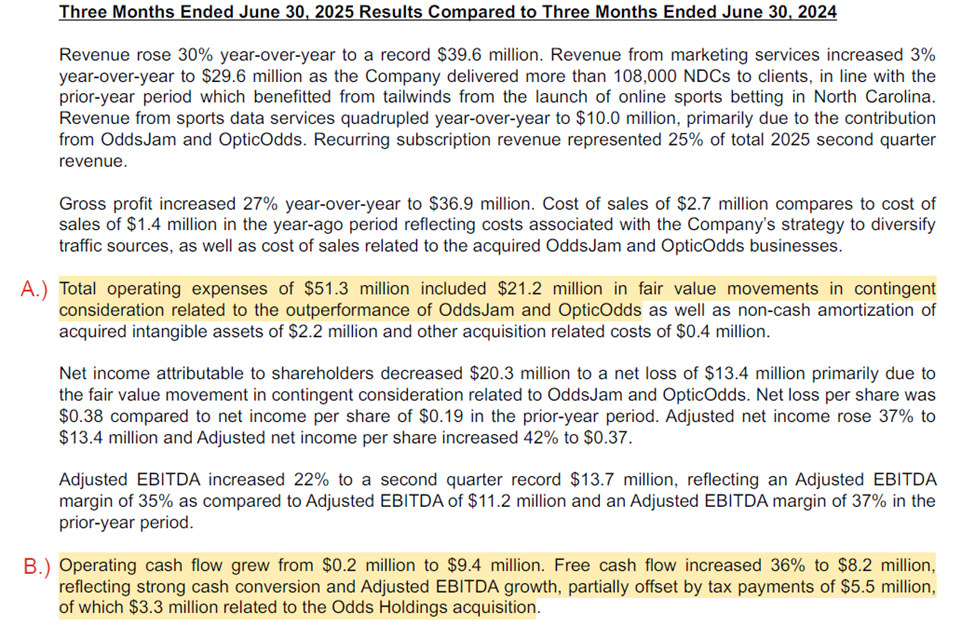

Gaming.com’s press release on August 14, 2025 confirms contingent consideration as the main culprit for the Q2 loss (Exhibit 4 – Note A).

This is a textbook case of an accounting loss having hardly any true current impact on business fundamentals. As the economist Alfred Rappaport notoriously said, “Cash is fact. Earnings are an opinion.” GAMB still generated free cash flow of $8.2 million in Q2 2025 (Exhibit 4 – Note B). Business fundamentals for GAMB remain strong, even though IFRS accounting shows a loss.

Reasoning for Use: GAMB utilizes contingent consideration as a way of aligning seller interest with the future performance, minimizing downside risk, and rewarding the seller for a smooth transition. Earnouts can also be used as a great negotiation tool. Sellers almost always overestimate and/or inflate the future potential of their company; therefore, deploying contingent consideration into a deal can communicate to the seller: “Sure, I’ll pay your asking price, but only if the returns materialize into the forecasted expectations over the next 2-3 years; otherwise, you only get the 50% upfront cost”.

The takeaway: Having to accrue this liability isn’t a sign of weakness; in fact, I believe it is a positive sign of a company displaying solid implementation and operations of acquisitions; the only reason GAMB would even be accruing for this liability would be because the 2024 Odds Holdings acquisition is exceeding expectations. In other words, the stock is being “punished” for successful execution and growth.

Valuation – Is GAMB Undervalued?

Balance Sheet & Capital Allocation Summary:

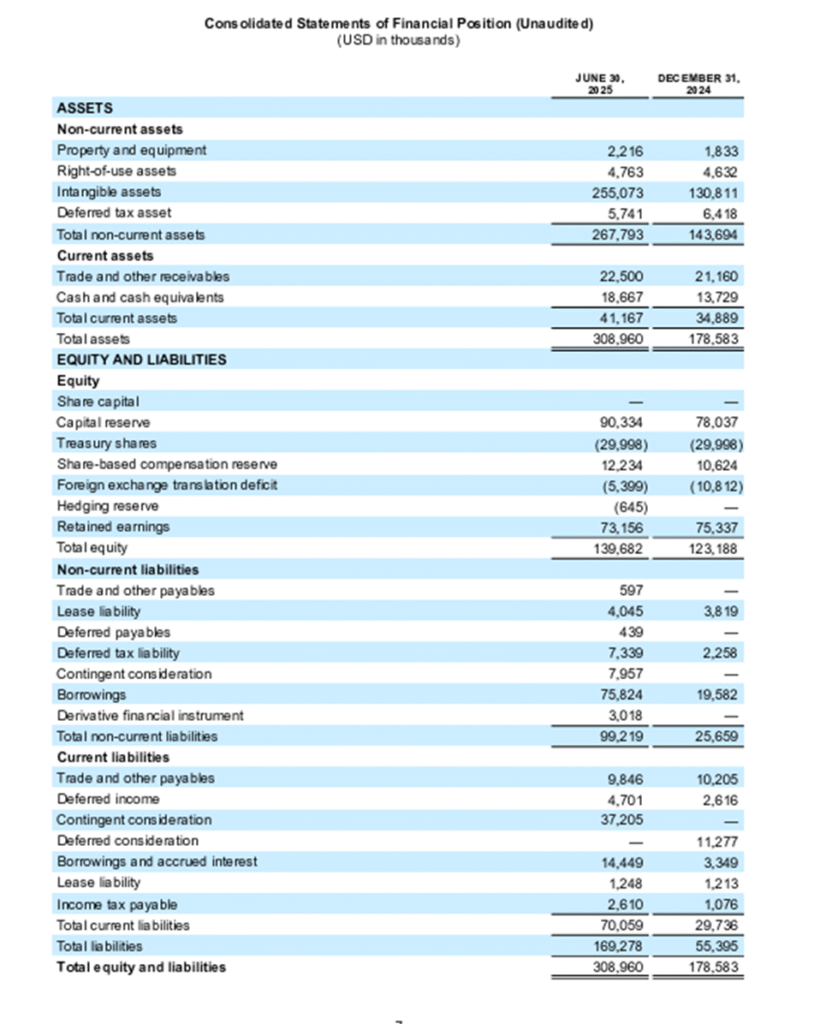

- Cash: $18.7 million

- Available credit: $70.5 million

- Buybacks: Recently doubled to $20 million

- Debt/Equity: 0.68

- Interest Coverage Ratio: 8.3x

- Foreseeable Future Acquisition Costs/Liabilities: Gambling.com expects to close the acquisition of Spotlight.Vegas (ticketing platform) in September 2025. The deal includes $8 million due at closing and an additional $22 million based on future benchmarks through 2027.

Valuation and Financial Forecast:

Revisiting the 2025 guidance from Q2 2025 earnings:

- Revenue: $171–175 million (midpoint +36% YoY)

- Adjusted EBITDA: $62–64 million (midpoint +29% YoY)

For valuation estimates, we will remain conservative with our figures. To project full year forecasted earnings (adjusted to exclude contingent consideration), we will take into consideration net income margin over the past two years.

I recognize there are many moving parts including changes in revenue, debt, margins, etc. between periods. I have also ran more sophisticated models which interesting enough landed us in a reasonably similar area when forecasting future income; therefore, for transparency and clarity sake, we will utilize the simpler model (i.e. trailing net income margin).

With that said, it is worth noting net income margins have been gradually increasing. Q1 2025 net income margin was 28%, while the 2024 full year net income margin came in at 24%. Therefore, to remain cautious with our forecast, we use the following conservative assumptions:

- Net income margin: 24%

- Shares outstanding: 35.71 million (finviz.com)

- Management’s Revenue Forecast for 2025: $171 million

Note: We are calculating FY 2025 EPS; not forward EPS which will likely be higher. Based on the figures above FY 2025 EPS is $1.15.

- Estimated Adjusted EPS 2025: $1.15

- Current GAMB Share Price: $8.61

- FY 2025 Forecasted P/E: 7.49

For a company which is growing Q2 YoY revenue by 36% and adjusted EBITDA by 22%, a P/E of 7.49 is an absurdly cheap valuation. It signals the market’s lack of confidence in sustainable growth. To continue to put this into perspective, we will now conduct a discounted cash flow model encompassing the following assumptions:

- Free Cash Flow: $36.8 million per year (FCF Q2 2025 of $8.2 million x 4 quarters)

- FCF/Share: $0.98 – which was rounded down from $1.03 to remain conservative

- FCF Annual Growth: 11% – even though adjusted EBITA is up 29% YoY

- Discount Rate: 12% – WACC is approximately 12%

- EV/EBITDA Exit Multiple: 6.50x (currently 6.45x)

- Growth Years: 10 years.

Even using these conservative assumptions, the FMV arrives at approximately $16.25 vs. $8.61 current price. That implies a Margin of Safety of approximately 47%. In other words, the stock price would need to double in order to reach this FMV estimate.

Take into consideration this FMV estimate is a forecast based on historic results. Results will obviously vary. In the following sections we will explore some risk factors and growth drivers which may cause this projection to fluctuate:

Long-Term Investment Case – Risk Factors

- SEO Ranking Recovery Uncertainty: If GAMB is unable to regain Google rankings within the next 2-3 months, the substitution of paid traffic will likely drag down margins.

- Regulatory Dependence: Delays in Missouri or other state launches could negatively impact the company achieving the current revenue guidance.

- IFRS Volatility: Future quarters may continue to show paper losses due to future contingent consideration revaluations.

- Future Earnout Payments: If all goes as planned with the implementation and execution of these newly acquired businesses, the remaining amount from the OddsJam/OpticOdds earnout will be due in 2026 along with an additional $22 million in 2027 from the Spotlight.Vegas acquisition. Although these accounting expenses are not currently affecting cash, there will come a time when these obligations need to be paid out in either cash or stock upon satisfying the performance metrics.

- Potential Future Shareholder Dilution: On August 14th, 2025, GAMB filed a Form F3 in order to be able to issue 6.7 million additional shares. Although this is not a direct offering, this creates flexibility for the company to issue new shares. It should also be noted that some of the terms from acquisitions utilizing contingent consideration include Gambling.com Group being able to settle a portion of payouts in company stock (e.g. up to 50% Odds Holding contingent consideration).

I will be the first to admit, I am usually opposed to dilution; but I also tend to focus on more mature companies. For a young growing company like GAMB to succeed, it is sometimes more responsible to issue equity rather than debt to fund operations/acquisitions; therefore, if management continues to structure buyouts in ways that minimize downside risk (i.e. earnouts), keeps executing well, and continues to exceed operational expectations, I would be fine with some dilution; so long as the money is used for funding solid acquisitions and expanding GAMB’s ecosystem to create synergies between product offerings.

Long-Term Investment Case – Growth Drivers

- Sports Data Expansion: Both OddsJam and OpticOdds create recurring, contract-based revenue. Sports data service revenue quadrupled to $10 million YoY in Q2 2025. If this unit continues to scale even another 2-3x, this could become a game changer; potentially leading to a rerating of GAMB’s valuation multiple.

- Geographic Growth: Each U.S. state launch of legalized sports betting (e.g. Missouri in December 2025) drives a spike in both NDCs and revenue share for Gambling.com.

- Diversification Beyond SEO: The Spotlight.Vegas acquisition expands GAMB into offline Vegas ticketing. It’s a diversified hedge against algorithm risk, indicating management at GAMB is moving away from exclusively relying on Google.

- Continued Growth in Subscription & Recurring Revenue: Subscription revenue now sits at 25% of overall revenue while recurring revenue made up 51% of total Q2 2025 revenue. Recurring revenue is a significant positive catalyst for both investors and the company’s outlook on future financing.

- Spotlight.Vegas Contributions: Scheduled to close in September 2025, the newly acquired Las Vegas ticketing and booking platform could immediately start adding a diverse revenue stream to GAMB. Spotlight.Vegas is projected to generate $8 million in revenue in FY2026 and adjusted EBITDA of $1.4 million.

Final Take

In my opinion, the IFRS net loss which triggered the -17% one day drop is more of a byproduct of success (overperforming acquisitions) than an indicator of a material fundamental business weakness.

On both a cash and adjusted earnings basis, Gambling.com remains a serious growth stock; with Q2 2025 YoY Revenues growing +30%, Gross Profit +27%, and Adjusted EBITDA +22%. Looking forward into H2 2025, many of the same drivers which contributed to the company’s solid performance and growth in H1 2025 remain.

Yes, GAMB stock is down -49% in the past six months… but as Peter Lynch once said: “The real key to making money in stocks is not to get scared out of them.”

Bottom Line – Is GAMB Undervalued?

For investors with the patience, temperament, and risk-tolerance for small-cap volatility, GAMB may be something worth considering. With its rare combination of high growth and a relatively low valuation multiple, I believe this selloff has created a buying opportunity. Weekly Investments rates this stock a BUY.

Disclosure

This article is for informational purposes only and does not constitute financial, investment, or any other form of professional advice. The views expressed are those of the contributor and are based on publicly available information and personal analysis.

The contributor holds positions in some or all of the investments mentioned, including Gambling.com Group (GAMB), and may benefit from any price appreciation discussed herein. This potential conflict of interest is disclosed for transparency.

No representation is made as to the accuracy or completeness of the information provided. Readers are solely responsible for verifying any facts and should consult a licensed financial advisor before making investment decisions. Past performance is not indicative of future results.